The pandemic has impacted household income and as such, affected the structure of household groups. But keep your heads up, everyone, for this may only be temporary as the economy improves and recovers from the pandemic.

In 2020, the Department of Statistics Malaysia (DOSM) found that the number of poor households increased to 639.8 thousand households compared to 405.4 thousand in 2019. Absolute poverty also increased from 5.6% (2019) to 8.4%. Because of this, household income classifications were also altered due to the drastic changes.

Income inequality also increased. Malaysia’s Gini Coefficient of gross income gradually rose to 0.41 (2021) from 0.407 (2019). Not that a higher value means more inequality which shows how hard the pandemic has hit and affected the range of what customers can and can’t afford.

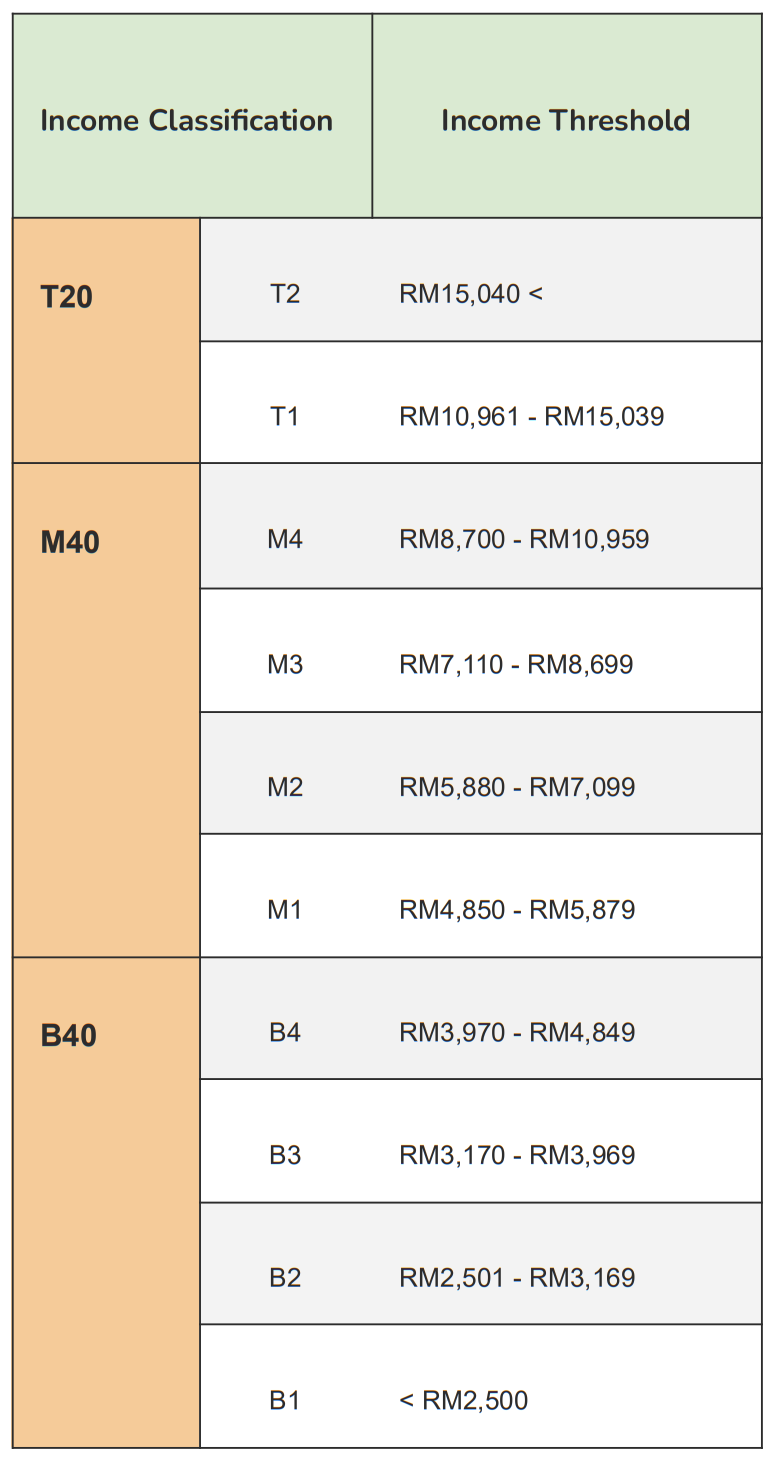

These classifications are made to help the government plan social security schemes and form development plans for the nation.

The pandemic’s financial impacts have created new household income classifications. Changes are not so drastic, but many households have dropped or hopped a tier, which affects their eligibility for government aid and housing schemes. For example, many bordering just outside the B40 category are now able to receive the available financial aid of B40 households.

Malaysia’s main sources of income are paid employment, self employment, and property & investment (DOSM). But in 2020, paid employment and self employment income values decreased by 16% and 9.7%. Overall, the mean monthly gross income for individuals fell by 10.3% and stood at RM7,089 compared to RM7,901 in 2019.

This was due to the reduction of income from reduced working hours to adhere to strict SOPs, and an increase in skill-related unemployment as many had to stay home.

Households shifted into lower groups.

In the year 2020 alone:

But look on the bright side! Many households that weren’t able to benefit from the financial support of the income levels below them are now able to do so. This makes purchasing property easier especially for households moving into the B40 category.

Now that you’re up to date with household income classifications, you can:

→ See your client’s eligibility for government schemes.

→ Know your client’s rough budget range.

→ Filter what your client absolutely can or can’t afford.

.svg)

.svg)